Why this matters now

If you still look at Saudi Arabia only as an oil exporter, you are already missing the bigger transition story. Riyadh is trying to move from being central to the old energy system into becoming strategically useful in the new one. That means lithium, copper, nickel, refining capacity, battery chemicals, EV factories, industrial land, and sovereign capital all need to be viewed together, not as isolated projects.

The phrase lithium monopoly is a strong hook, but it is too aggressive if we want to stay honest with investors. Saudi Arabia does not control global lithium mining and it does not dominate battery refining. What it is actually doing is more subtle and, in many ways, more important. It is trying to secure strategic leverage across the future EV supply chain while the market still underestimates how much value can sit in processing, logistics, and energy-backed industrial infrastructure.

Lithium prices have already taught the market an important lesson. Even with a long-term EV growth story, the commodity itself can go through deep boom-and-bust cycles. That is exactly why this Saudi move matters now. States with patience usually prefer to build during weak cycles, when assets are cheaper, sentiment is colder, and private competition is less willing to spend aggressively.

Saudi Arabia does not need this story to work next quarter. It needs this strategy to matter over the next ten to fifteen years. That is a completely different time horizon from what many listed miners, battery companies, or EV manufacturers can tolerate. That longer horizon is one of Riyadh’s biggest competitive advantages.

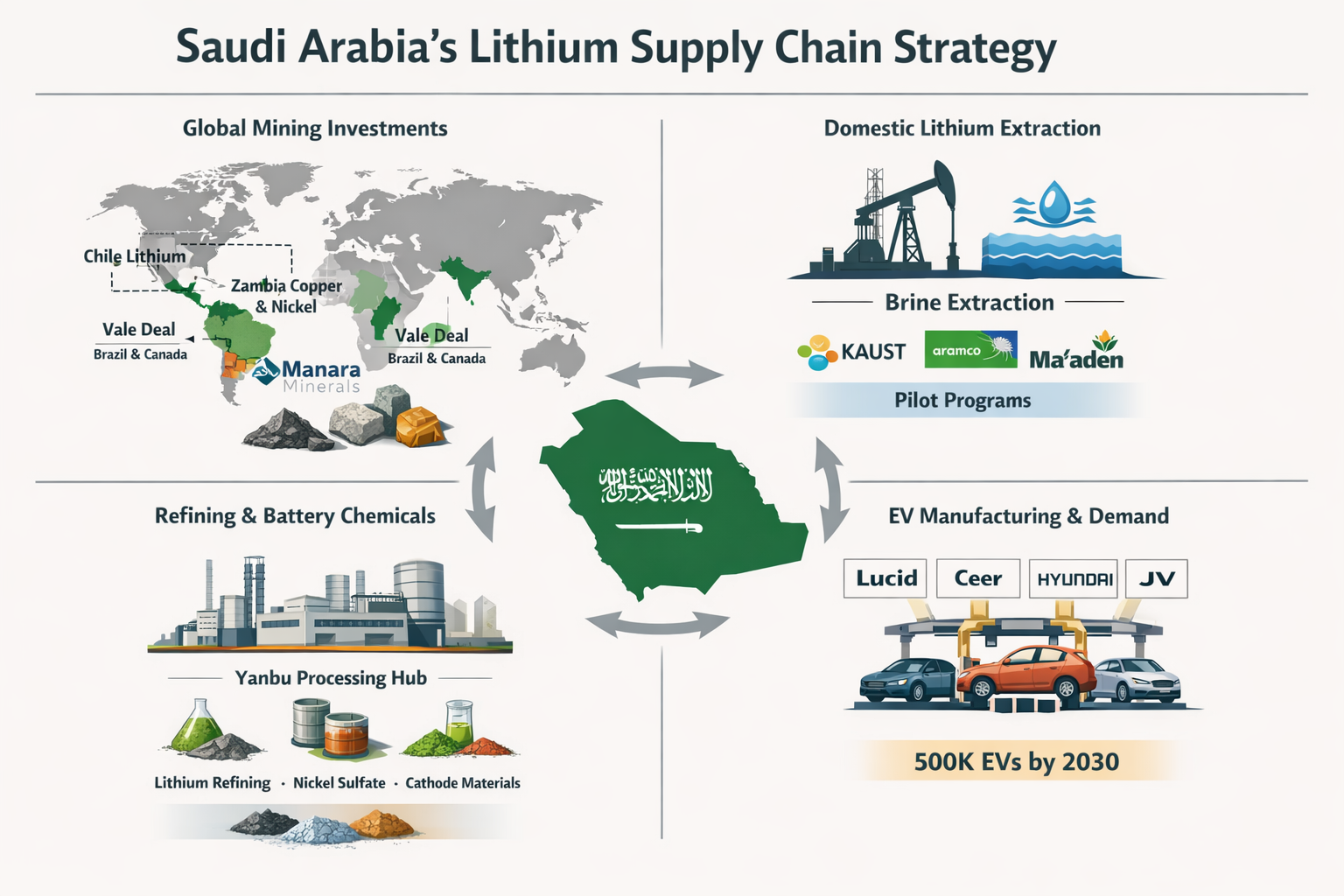

Saudi Arabia’s lithium supply chain strategy

The Saudi plan is strongest when you stop seeing it as a single-metal trade and instead view it as a multi-layer industrial strategy. There are four linked components that make the thesis powerful.

First, overseas mineral access. Saudi Arabia understands that future battery security begins far before the battery factory. That means taking stakes, forming partnerships, or building influence in upstream assets tied to lithium, copper, nickel, and related metals. Serious supply chain strategy is never only about lithium because an EV battery and the supporting grid ecosystem depend on multiple inputs.

Second, domestic extraction experiments. This is where the story becomes more intriguing. Saudi Arabia is exploring lithium extraction from brines and other high-salinity sources connected to its energy ecosystem. If that becomes commercially viable, the country moves from being only a capital allocator into also becoming a real domestic source of strategic material. But investors need discipline here: pilot success is not the same as scalable economics.

Third, refining and battery chemicals. This may become the most valuable layer. Mining gets the headlines, but refining often captures the strategic choke point. Saudi Arabia has cheap energy, industrial zones, export infrastructure, chemicals experience, and strong state backing. If it becomes a trusted processor of battery-grade material, it can gain importance without owning every mine.

Fourth, downstream demand creation. By supporting EV assembly, industrial ecosystem buildout, and logistics corridors at home, Riyadh is not just building supply. It is also trying to create local demand and supplier clustering. That is how industrial strategies become sticky and harder for competitors to displace.

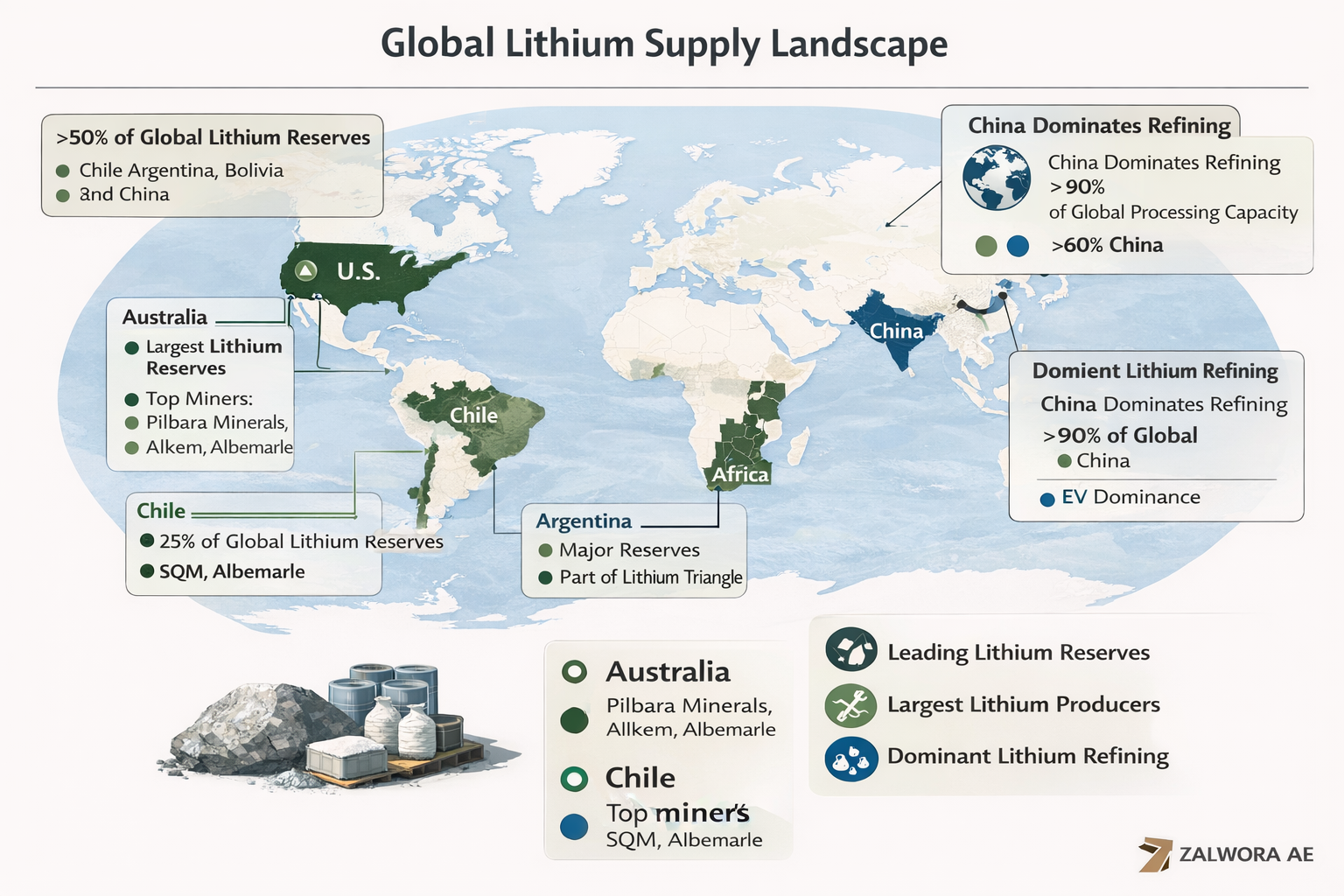

The global lithium map explains why Riyadh is moving

Lithium is not evenly distributed. The market is geographically concentrated, politically sensitive, and deeply influenced by who refines material at scale. That concentration is one reason countries are now treating critical minerals as instruments of industrial security, not just commodities.

For Saudi Arabia, this creates an opening. If the global market is uncomfortable with excessive concentration in a few places, then a well-capitalized Gulf industrial hub can present itself as a credible alternative partner. It will not replace the incumbents overnight, but it can become valuable as a diversification node. In markets, being the alternative can still be extremely profitable.

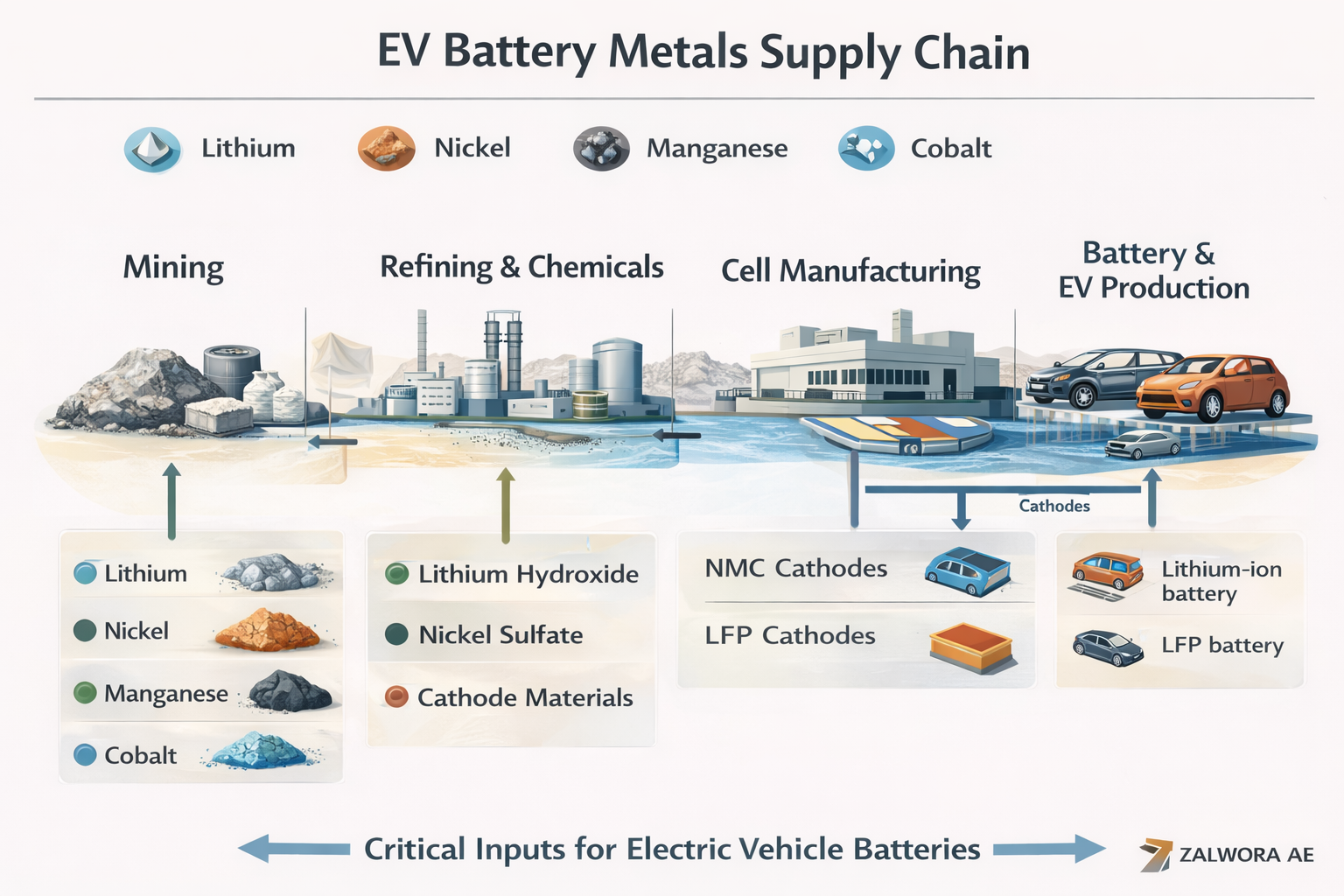

Why lithium is only one part of the battery story

One of the biggest mistakes retail investors make is treating lithium like the entire EV story. It is not. The future battery economy is a chain made of mining, refining, chemicals, cell manufacturing, pack assembly, vehicle production, grid storage, logistics, and energy availability. Whoever wants lasting influence must understand the whole chain.

This is why Saudi Arabia’s approach is more sophisticated than it first appears. It is not merely chasing a hot commodity. It is trying to insert itself where supply chains become strategic. A country that can offer capital, energy, land, refining, and shipping infrastructure may become more useful to the battery ecosystem than a country that only has geology.

Why sovereign wealth changes the game

Private investors often become cautious when commodity prices fall. Sovereign wealth does not have to behave the same way. This is where Saudi Arabia becomes harder to dismiss. It can deploy money across mining, refining, logistics, and industrial infrastructure with a much longer time horizon than most commercial players. In simple words, it can continue building through periods that would shake out weaker private capital.

That does not mean the strategy is risk free. It means the country can absorb complexity for longer than most competitors. Instead of asking whether one specific mine looks attractive in isolation, it can ask whether an entire corridor of future industrial relevance is worth owning a piece of.

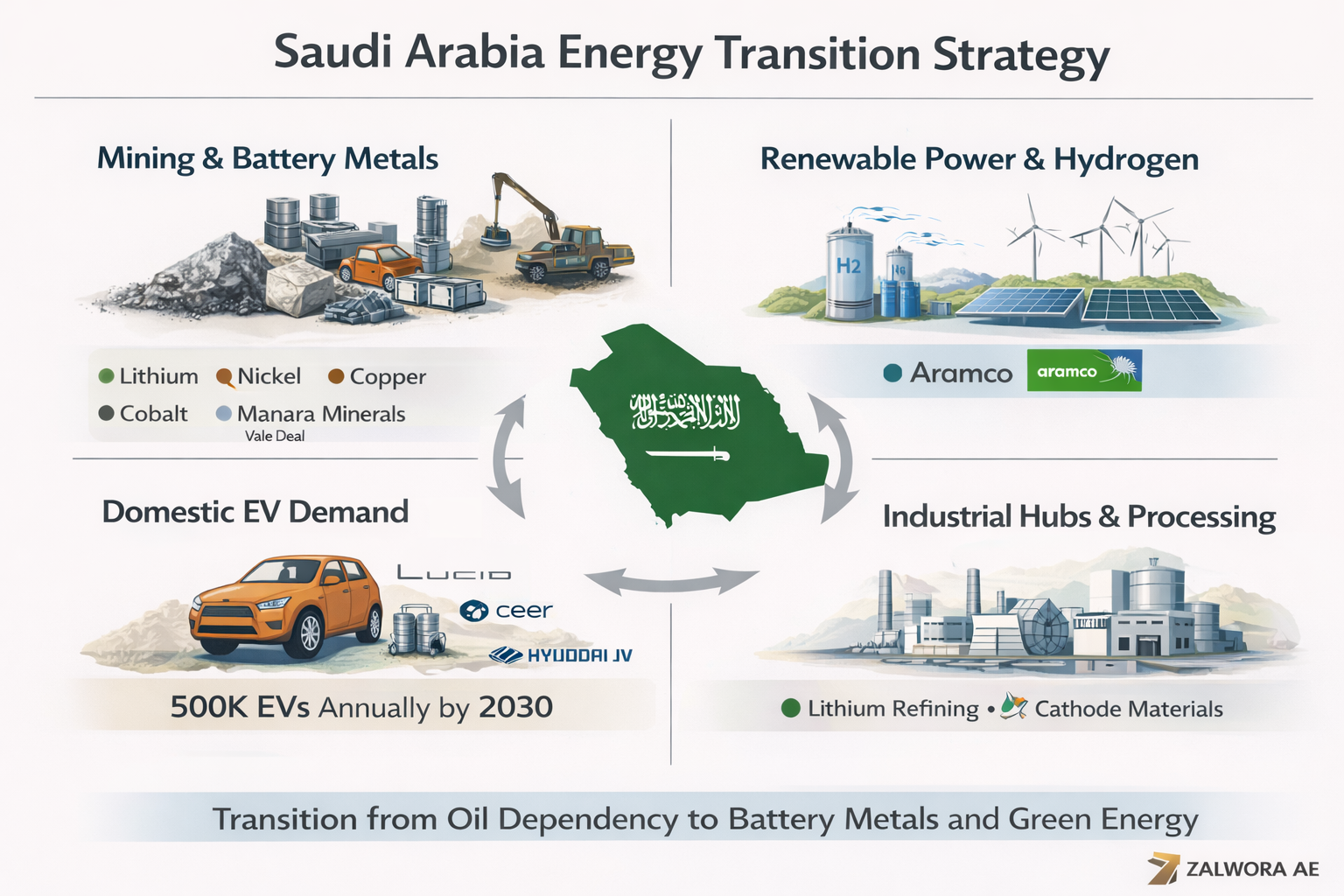

The macroeconomic power shift behind the story

This is not just about EVs. It is about future power. For decades, Gulf relevance came from hydrocarbons. In the coming era, countries that combine energy abundance, industrial land, processing capacity, metals access, logistics, and patient capital may remain central even if the energy mix shifts. Saudi Arabia understands that clearly.

In other words, the Kingdom is trying to avoid a future where the world electrifies and Saudi Arabia becomes less relevant. Instead, it wants to stay inside the system by helping power the industries that replace or complement fossil fuel demand. That is why this should be viewed as a macro pivot, not just a mining headline.

So is this really a monopoly story?

No, not today. The stronger and more realistic interpretation is that Saudi Arabia wants to become too important to ignore in the future battery chain. That is a very different claim, and a much more investable one.

China still has scale, cost advantages, and deep refining capacity. Global lithium remains cyclical, politically sensitive, and vulnerable to oversupply phases. Saudi domestic lithium is still an emerging story, not a mature one. So the word monopoly is best understood as a dramatic framing device, not a literal description of the market.

But dismissing the Saudi move would be a mistake too. Countries do not need to own 100 percent of a resource to gain leverage. They only need to occupy a strategic layer that others depend on. Processing, industrial trust, and supply chain diversification can be just as valuable as raw reserves.

The bullish case and the bearish case

The bull case is straightforward. If Saudi Arabia can convert domestic extraction pilots into economic reality, deepen overseas mineral ownership, build credible refining capacity, and connect all of that to a growing EV and industrial ecosystem, it could become one of the most important emerging battery-metal hubs outside the traditional centers.

That would not necessarily make it the global king of lithium. But it could make it one of the most influential strategic nodes in the chain, especially if governments and manufacturers continue prioritizing supply security and diversification.

The bear case deserves equal respect. Lithium oversupply can last longer than expected. New battery chemistries can reduce demand intensity for some inputs. Pilot extraction may fail to deliver attractive economics at scale. Refining is highly competitive. Supplier ecosystems are much harder to build than announce. And the more layers of an industrial strategy being built at once, the higher the execution risk.

My final conclusion

Saudi Arabia is not building a lithium monopoly yet. But it is building a serious and intelligent battery-metals strategy that deserves attention from investors, policymakers, and anyone tracking future industrial power. The real advantage is not only geology. It is the combination of sovereign wealth, policy alignment, industrial infrastructure, cheap energy, and patience.

The right investor framing is this: too early to call dominance, too important to ignore, and potentially one of the most significant long-term supply chain stories in the Middle East over the next decade.

What investors should watch next

1. New overseas acquisitions

Watch for more stakes or partnerships tied to lithium, copper, nickel, and strategic refining assets.

2. Domestic pilot milestones

The biggest proof point is whether Saudi lithium extraction moves from interesting pilot headlines to commercial economics.

3. Refining and chemical execution

Announcements matter less than actual buildout, feedstock sourcing, processing scale, and customer trust.

4. EV ecosystem traction

Real manufacturing volumes, local suppliers, and industrial clustering will matter more than press releases.

5. Global lithium cycle

If the market tightens again after a long weak phase, Saudi positioning may suddenly look much more valuable.

6. Geopolitical partnerships

Critical mineral partnerships with Western and Asian players can increase Saudi relevance beyond the mining sector alone.

Research note: This article is written as a simplified investor opinion piece based on public reporting, company announcements, and market analysis around Saudi Arabia’s critical minerals, battery metals, and EV supply chain strategy as of March 8, 2026.